Information for Kentucky Homebuyers

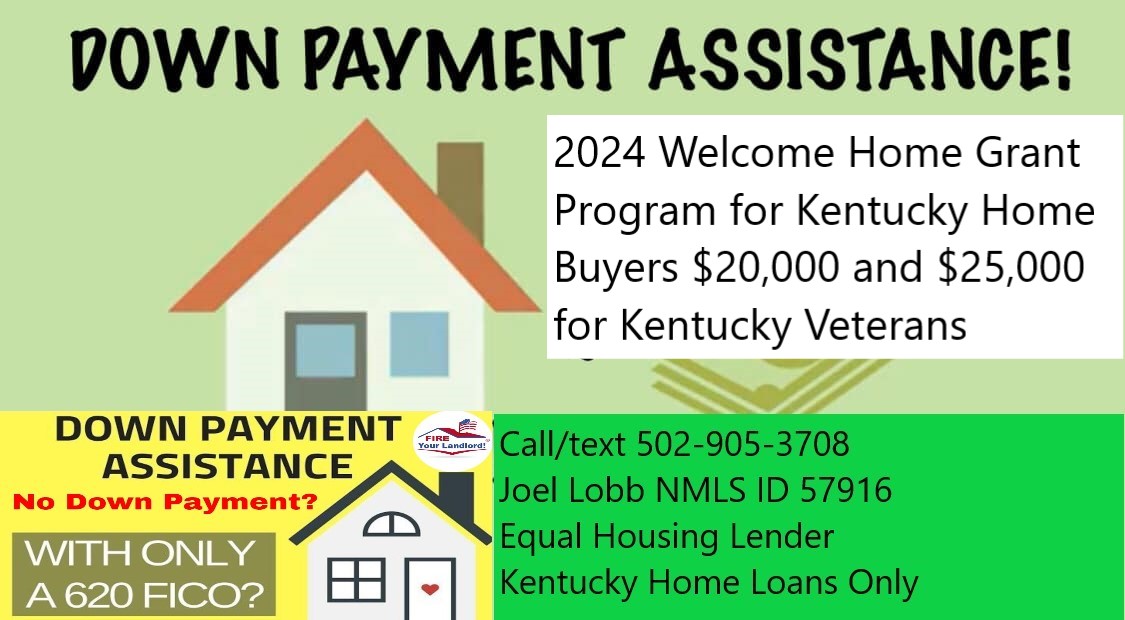

Welcome Home Program Grant Program for Kentucky Home buyers in 2024

The Federal Home Loan Bank of Cincinnati (FHLB Cincinnati) offers grants of up to $25,000 for honorably discharged veterans, surviving spouses of military personnel, and active duty military homebuyers and up to $20,000 for all other homebuyers to assist with down payment and closing costs for income eligible homebuyers through the Welcome Home Program (WHP).

Kentucky Homebuyers must apply and qualify for a mortgage loan with one of our Member financial institutions to utilize the grant.

Who are Eligible Homebuyers in Kentucky for the Welcome Grant?

A Kentucky homebuyer would be eligible for the Welcome Home grant if all of the following guidelines are met:

The total income for all occupants who will reside in the home is at or below 80 percent of the Mortgage Revenue Bond (MRB) limit for the county and state where the property is located;

A fully executed (signed by buyer and seller) purchase contract on an eligible property is in hand;

The homebuyer has at least $500 of their own funds to contribute towards down payment and/or closing costs; and,

If a first-time homebuyer (typically anyone who has not owned a home in the last three years), a satisfactory homebuyer counseling course is completed prior to the loan closing. Note: Applicants do not have to be first-time homebuyers.

A fully executed (signed by buyer and seller) purchase contract on an eligible property is in hand;

The homebuyer has at least $500 of their own funds to contribute towards down payment and/or closing costs; and,

If a first-time homebuyer (typically anyone who has not owned a home in the last three years), a satisfactory homebuyer counseling course is completed prior to the loan closing. Note: Applicants do not have to be first-time homebuyers.

What is an Eligible Property?

A property would be eligible if all of the following guidelines are met:

The property will be the homebuyer’s primary residence;

The property is a single family, townhome, condominium, duplex, multi-unit (up to four family units) or a qualified manufactured home. (Manufactured homes may be eligible if they are taxed as real estate and affixed to a permanent foundation); and,

The property is subject to a legally enforceable five-year retention mechanism, included in the Deed or as a Declaration of Restrictive Covenants to the Deed, requiring the FHLB Cincinnati be given notice of any refinancing, sale, foreclosure, deed in-lieu of foreclosure, or change in ownership during the five year retention period.

The property is a single family, townhome, condominium, duplex, multi-unit (up to four family units) or a qualified manufactured home. (Manufactured homes may be eligible if they are taxed as real estate and affixed to a permanent foundation); and,

The property is subject to a legally enforceable five-year retention mechanism, included in the Deed or as a Declaration of Restrictive Covenants to the Deed, requiring the FHLB Cincinnati be given notice of any refinancing, sale, foreclosure, deed in-lieu of foreclosure, or change in ownership during the five year retention period.

How Do I Apply?

For more program information, homebuyers should contact a FHLB Cincinnati Member financial institution.

A list of Members is available at List of Kentucky Mortgage Lenders for the Welcome Grant Home Program for $20,000 for 2024 KY Homebuyers

List of Kentucky Mortgage Lenders for the Welcome Grant Home Program for $20,000 for 2024 KY Homebuyers

List of Kentucky Mortgage Lenders for the Welcome Grant Home Program for $20,000 for 2024 KY HomebuyersKentucky has many programs and grants for first-time home buyers with no money down home loans and down payment assistance programs for 2024

,see list below and let me know if you have any questions at 502-905-3708– call or text

or email me at kentuckyloan@gmail.com

LIST BELOW

- HUD Community Development Block Grants (CDBG) — Kentucky contacts: HUD provides grant money to communities and those funds may be used to assist home buyers

- HUD HOME Program — Kentucky contacts: HUD provides grant money to communities designated as participating jurisdictions for assisting home buyers, rental assistance, and other housing initiatives

- Community Ventures Corporation Kentucky Home Financing

- The Kentucky Housing Corporation offers:

- Habitat for Humanity: Through volunteer labor and donations of money and materials, Habitat builds and rehabilitates simple, decent houses with the help of the homeowner (partner) families

- Federal Home Loan Bank of Cincinnati: Serves Kentucky residents by offering various home buying assistance programs, including Welcome Home grants. For more information, you may call 1 (888) 345-2246

- Kentucky Area Development Districts (ADDs): Contact your local ADD to find out more about local home buying assistance programs

- Kentucky Association for Community Action: Helps to fund housing programs for low-income residents

- Federal Appalachian Housing Enterprise (FAHE): Provides housing assistance in rural, low-income, Appalachian communities

- Housing Partnership, Inc.: Provides affordable housing services for residents of Jefferson County

- Secondary financing/down payment assistance programs are listed by state

- USDA Rural Development: Home buying loan programs that reduce the cost of homeownership for low and moderate-income families

Ask your loan officer about these program

Kentucky Income Limits for Welcome Home Grant in 2024

Use the 80% Limits, not the 100% Limits

Each Kentucky county is listed below

1-2 person households

and 3+person households

| 100% limits | 80% limits**** Use this | |||||

| 1-2 Persons | 3 + Persons | 1-2 Persons | 3 + Persons | |||

| Adair | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 | ||

| Allen | $ 78,600 | $ 91,420 | $ 62,880 | $ 73,136 | ||

| Anderson | $ 86,270 | $ 99,210 | $ 69,016 | $ 79,368 | ||

| Ballard | $ 80,400 | $ 93,800 | $ 64,320 | $ 75,040 | ||

| Barren | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 | ||

| Bath | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Bell | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Boone | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 | ||

| Bourbon | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 | ||

| Boyd | $ 83,040 | $ 96,880 | $ 66,432 | $ 77,504 | ||

| Boyle | $ 80,760 | $ 94,220 | $ 64,608 | $ 75,376 | ||

| Bracken | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 | ||

| Breathitt | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Breckinridge | $ 87,410 | $ 100,521 | $ 69,928 | $ 80,417 | ||

| Bullitt | $ 89,700 | $ 103,155 | $ 71,760 | $ 82,524 | ||

| Butler | $ 78,600 | $ 91,420 | $ 62,880 | $ 73,136 | ||

| Caldwell | $ 84,480 | $ 98,560 | $ 67,584 | $ 78,848 | ||

| Calloway | $ 82,560 | $ 96,320 | $ 66,048 | $ 77,056 | ||

| Campbell | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 | ||

| Carlisle | $ 78,600 | $ 90,860 | $ 62,880 | $ 72,688 | ||

| Carroll | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 | ||

| Carter | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Casey | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Christian | $ 87,590 | $ 100,728 | $ 70,072 | $ 80,582 | ||

| Clark | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 | ||

| Clay | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Clinton | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| Crittenden | $ 83,760 | $ 97,720 | $ 67,008 | $ 78,176 | ||

| Cumberland | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 | ||

| Daviess | $ 86,950 | $ 99,992 | $ 69,560 | $ 79,994 | ||

| Edmonson | $ 86,650 | $ 99,647 | $ 69,320 | $ 79,718 | ||

| Elliott | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 | ||

| County | 100% limits | 80% limits | ||

| 1-2 Persons | 3 + Persons | 1-2 Persons | 3 + Persons | |

| Estill | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Fayette | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 |

| Fleming | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Floyd | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Franklin | $ 85,430 | $ 98,244 | $ 68,344 | $ 78,595 |

| Fulton | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Gallatin | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 |

| Garrard | $ 87,210 | $ 100,291 | $ 69,768 | $ 80,233 |

| Grant | $ 79,560 | $ 92,820 | $ 63,648 | $ 74,256 |

| Graves | $ 83,160 | $ 97,020 | $ 66,528 | $ 77,616 |

| Grayson | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Green | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Greenup | $ 83,040 | $ 96,880 | $ 66,432 | $ 77,504 |

| Hancock | $ 86,950 | $ 99,992 | $ 69,560 | $ 79,994 |

| Hardin | $ 86,750 | $ 99,762 | $ 69,400 | $ 79,810 |

| Harlan | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Harrison | $ 87,250 | $ 100,337 | $ 69,800 | $ 80,270 |

| Hart | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Henderson | $ 87,300 | $ 100,395 | $ 69,840 | $ 80,316 |

| Henry | $ 89,700 | $ 103,155 | $ 71,760 | $ 82,524 |

| Hickman | $ 79,560 | $ 92,820 | $ 63,648 | $ 74,256 |

| Hopkins | $ 80,640 | $ 94,080 | $ 64,512 | $ 75,264 |

| Jackson | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Jefferson | $ 89,700 | $ 103,155 | $ 71,760 | $ 82,524 |

| Jessamine | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 |

| Johnson | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Kenton | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 |

| Knott | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Knox | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Larue | $ 86,750 | $ 99,762 | $ 69,400 | $ 79,810 |

| Laurel | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Lawrence | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Lee | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Leslie | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Letcher | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Lewis | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Lincoln | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Livingston | $ 82,320 | $ 96,040 | $ 65,856 | $ 76,832 |

| Logan | $ 80,760 | $ 94,220 | $ 64,608 | $ 75,376 |

| Lyon | $ 87,310 | $ 100,406 | $ 69,848 | $ 80,325 |

| County | 100% limits | 80% limits | ||

| 1-2 Persons | 3 + Persons | 1-2 Persons | 3 + Persons | |

| McCracken | $ 87,130 | $ 100,199 | $ 69,704 | $ 80,159 |

| McCreary | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| McLean | $ 86,950 | $ 99,992 | $ 69,560 | $ 79,994 |

| Madison | $ 86,910 | $ 99,946 | $ 69,528 | $ 79,957 |

| Magoffin | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Marion | $ 80,760 | $ 94,220 | $ 64,608 | $ 75,376 |

| Marshall | $ 86,030 | $ 98,934 | $ 68,824 | $ 79,147 |

| Martin | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Mason | $ 85,920 | $ 100,240 | $ 68,736 | $ 80,192 |

| Meade | $ 85,790 | $ 98,658 | $ 68,632 | $ 78,926 |

| Menifee | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Mercer | $ 86,730 | $ 99,739 | $ 69,384 | $ 79,791 |

| Metcalfe | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Monroe | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Montgomery | $ 78,600 | $ 91,140 | $ 62,880 | $ 72,912 |

| Morgan | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Muhlenberg | $ 78,600 | $ 91,700 | $ 62,880 | $ 73,360 |

| Nelson | $ 85,170 | $ 97,945 | $ 68,136 | $ 78,356 |

| Nicholas | $ 78,600 | $ 90,860 | $ 62,880 | $ 72,688 |

| Ohio | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Oldham | $ 89,700 | $ 103,155 | $ 71,760 | $ 82,524 |

| Owen | $ 78,600 | $ 91,700 | $ 62,880 | $ 73,360 |

| Owsley | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Pendleton | $ 101,100 | $ 116,265 | $ 80,880 | $ 93,012 |

| Perry | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Pike | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Powell | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Pulaski | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Robertson | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Rockcastle | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Rowan | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Russell | $ 78,600 | $ 90,860 | $ 62,880 | $ 72,688 |

| Scott | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 |

| Shelby | $ 92,700 | $ 106,605 | $ 74,160 | $ 85,284 |

| Simpson | $ 82,920 | $ 96,740 | $ 66,336 | $ 77,392 |

| Spencer | $ 89,700 | $ 103,155 | $ 71,760 | $ 82,524 |

| Taylor | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Todd | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Trigg | $ 87,590 | $ 100,728 | $ 70,072 | $ 80,582 |

| Trimble | $ 86,770 | $ 99,785 | $ 69,416 | $ 79,828 |

| County | 100% limits | 80% limits | ||

| 1-2 Persons | 3 + Persons | 1-2 Persons | 3 + Persons | |

| Union | $ 78,600 | $ 91,420 | $ 62,880 | $ 73,136 |

| Warren | $ 86,650 | $ 99,647 | $ 69,320 | $ 79,718 |

| Washington | $ 87,090 | $ 100,153 | $ 69,672 | $ 80,122 |

| Wayne | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Webster | $ 78,600 | $ 90,390 | $ 62,880 | $ 72,312 |

| Whitley | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Wolfe | $ 94,320 | $ 110,040 | $ 75,456 | $ 88,032 |

| Woodford | $ 89,300 | $ 102,695 | $ 71,440 | $ 82,156 |

You must be logged in to post a comment.